AUD

AUD

Loading... Please wait...

Loading... Please wait...

Recent Posts

Bond Market Crisis Will Crack the Silver Market Price Ceiling

Posted by on

The emergence of the current crisis in bond markets across the world will have dramatic implications for not only future economic policy, but also for global commodity and precious metals markets, especially the gold and silver market.

As noted in early February 2021 via the article “The Biden Administration will Accelerate Stagflation”[1], the economic policies of the Biden Administration will accelerate the stagflation phenomenon in the US that commenced under the Trump Administration.

These economic policies include:

- massive fiscal stimulus and additional government spending, including a proposed $US 1.9 trillion stimulus package and a $US 2 trillion (over 4 years) spending package to address climate change, cleaner energy and infrastructure requirements; and

- job destroying regulations, such as re-joining the Paris Climate Accord, cancelling major construction projects (e.g. the Keystone XL pipeline and the US-Mexico border wall), prohibiting fracking on federal government land as well as raising the minimum wage to $US 15 per hour.

Accelerated stagflation will manifest itself in various ways including:

- increased expectations of future inflation;

- rising commodity prices such as crude oil, base metals such as copper and iron ore, raw materials such as lumber as well as agricultural products such as grain; and

- rising bond yields resulting from existing portfolio holdings of government bonds being liquidated and weaker private sector demand for newly issued government bonds.

Bond Market Crisis

This last point of rising bond yields has unexpectedly emerged in the week commencing 22 February 2021 with rapid speed, which has caught both financial markets and policy makers off guard.

Concerns that unprecedented COVID-19 pandemic-related economic stimulus will lead to rising inflation and possibly stagflation, even once COVID-19 lockdown policies are relaxed, have been building among investors of government bonds for several months, but have now come to ahead.

The epicentre of the bond market crisis commenced in the United States (US) but quickly spread to other major bond markets in countries such as the Australia, Japan and Germany.

United States

As reported by CNBC,[2] the yield on 10-year US Government Bonds (US Treasuries) exploded to 1.6% on 25 February 2021 on fears that stagflation may be emerging, as opposed to a robust broad‑based economic recovery.

These fears led to a failure at a bond auction of 7-year US Treasuries held on 25 February 2021. As reported by Zero Hedge,[3] the “bid-to-cover ratio”[4] for the auction came in at 2.045 - the lowest on record, signalling weak demand for US government debt.

A major factor of this auction weakness was foreign buyers (known as “indirects”) whose demand for the bond issuance plunged from 64.10% to 38.01%, the lowest level since 2014, resulting in bond dealers being required to purchase 39.81% of the issuance - the highest since 2014.

Record economic stimulus in 2020 by the former Trump administration, coupled with the accelerated stagflation policies of the Biden Administration and political instability resulting from the conduct of American public policy by Washington DC politicians and officials, are likely factors as to why foreign investors are less inclined to purchase US Treasuries, especially at current yields.

Australia

As reported by Zero Hedge[5] on 25 February 2021, the Reserve Bank of Australia’s (RBA’s) yield curve control (YCC) policy of keeping the yield on 3-year Australian Government Bonds at a target rate of 0.1% began to unravel as inflation concerns began to take hold within the Australian bond market.

As the yield began to rise to 0.15%, the RBA was forced to intervene on three separate occasions[6] to keep the integrity of its 3‑year bond yield target intact. This includes purchases of 3-year Australian Government bonds of $AUD 1 billon on 22 February, $AUD 3 billion on 24 February and a further $AUD 3 billion on 26 February 2021.

Concerningly, volatility on the yield of 3-year Australian Government Bonds did not subside at the beginning of the following week on 1 March 2021, triggering the RBA to announce a doubling of its daily bond program from $AUD 2 billion per day to $AUD 4 billion per day[7].

Moreover, concerns regarding inflation and the lack of demand for Australian Government debt led to the Australian Office of Financial Management activating the Securities Lending Facility[8] facilitating the purchase of $AUD 450 million worth of bonds on 24 and 26 February 2021 at subsidised prices.

Importantly, problems in the Australian bond market were not just limited to 3-year bonds, but also manifested itself among 10-year Australian Government bonds as well.

Within the space of 5 months, bond yields on Australian Government 10-year bonds have risen by more than 2.5 times from 0.72% on 15 October 2020 to a high of 1.871% on 25 February 2021. As noted by Australian Financial Review (AFR) columnist Christopher Joye, this rise in Australian Government bond yields was faster than other developed countries.[9]

These developments come on the heels of the RBA’s early-February 2021 announcement to launch a second round of quantitative easing (QE) worth $AUD 100 billion once the current $AUD 100 billion round of QE concludes in April 2021.[10]

At the time of writing on 2 March 2021, the RBA Governor announced the Monetary Policy Decision of the RBA Board’s March meeting[11] indicating that:

- the RBA Board remains committed to its YCC target of 0.1% on 3-year Australian Government bonds;

- the RBA is ready to inject a third tranche of QE once the first two $AUD 100 billion tranches (as mentioned above) were exhausted; and

- accommodative monetary policy was expected to remain until 2024.

Japan

As reported by Zero Hedge,[12] yields on 10-year Japanese Government Bonds rose sharply on 25 February 2021 to 0.18%, the highest since early 2016, and in contradiction to the YCC target set by the Bank of Japan “of around zero percent”.

Germany

As reported by Reuters,[13] the yield on 10-year German Government bonds also spiked reaching ‑0.203% on 26 February 2021, almost tripling from its rate of -0.637% recorded on 11 December 2020.

Immediate Central Bank Policy Response

The emergence of the current bond market crisis provides a catalyst for central banks to clarify their “forward guidance” (i.e., their stated policy intention) as well as implement additional policy steps.

As noted by Bank of America,[14] financial markets (both bonds and equity markets) are now requiring, if not demanding, that central banks take additional steps to provide reassurance. given the turmoil of recent weeks.

Given the market turmoil, failure of central banks to revise their forward guidance and implement an appropriate policy response will see:

- bond yields continuing to climb as demand for fixed income financial instruments, such as government bonds (both in the primary and secondary bond market), fall;

- a sharp fall in the value of share market equities (and potentially a share market collapse) as the risk-free cost of capital rises;

- rising borrowing costs across the global financial system for financial institutions (including banks), non-financial corporations, households and governments;

- the emergence of defaults on existing debt obligations which, given the scale of the current global debt bubble, will lead to financial contagion and market panic; and

- financial contagion culminating in a new global financial crisis that will trigger the largest deflationary depression in human history (as predicted by famous deflationists such as Harry Dent).

During the past 13 years, economic policy makers (including central bank officials) across the world have implemented the most extreme form of fiscal and monetary policy stimulus to avoid a worldwide deflationary depression at critical points such as at:

- September 2008 - during the Global Financial Crisis;

- February 2012 - during the commencement of the Greek debt crisis;

- October 2018 – during the Italian debt crisis;[15]

- January 2019 - following a sharp fall in the US share market in December 2018;[16]

- September 2019 - the crisis in the US repo market; and

- March 2020 - during the contagion of the COVID-19 pandemic on financial markets.

Given this record, it is highly unlikely that these economic policy makers and central banks officials will now reverse course on macroeconomic policy, or allow market forces to overwhelm the intent of existing policy settings.

- Rather, if recent economic policy and the behaviour of governments and central banks are any guide, we are likely to witness an even greater amount of fiscal and monetary stimulus.

- Indeed, as reported by the AFR,[17] an international meeting of finance ministers over the weekend of 27‑28 February 2021, US Treasury Secretary Janet Yellen urged member countries to continue pursuing:

- “…significant fiscal and financial policy actions and avoid withdrawing support too early”.

- Yellen also stated that, “…If there was ever a time to go big, this is the moment.”

In the case of the US, additional economic stimulus will likely result in the US Federal Reserve embracing YCC as has been noted by several US analysts in recent weeks[18][19][20].

Alternatively, while countries such as Australia and Japan already have implemented YCC at the short end of the yield curve, other policy options to contain escalating bond yields may include:

- increasing the size of existing QE programs; and

- expanding YCC to include other points of the yield curve by including longer-term maturities.

Added Pressure to the Physical Silver Market

Importantly, when considering the potential policy impact of YCC being implemented in the United States, it should be noted that YCC was a key policy tool implemented during World War 2 in order to assist in the financing of the American war effort.

As noted by Bloomberg:[21]

“The Fed and the U.S. Treasury agreed in 1942 to cap borrowing costs to fund the country’s participation in World War II. Five years later, inflation was in double digits amid the post-war boom and the central bank was forced to start pulling back.”

Thus, additional economic stimulus measures such as implementing or expanding YCC, or expanding existing QE programs, will likely prove to be inflationary and result in further weakness of fiat currencies, especially currencies not tied to global commodities cycles such as the US dollar.

This weakness will in turn lead to further flight to commodities including precious metals such as physical gold and silver.

The flight to precious metals will not be isolated to one region of the world, but will be likely be a phenomenon of global dimensions given that:

- the bond market crisis has emanated from the US (the largest global bond market)[22] and thus will impact the entire global financial system;

- central bank policy across the world tends to be of a globally coordinated nature (especially between the US Federal Reserve, the European Central Bank and the Bank of Japan); and

- significant quantities of US dollar denominated assets are held, not only by Americans, but also by foreign investors.

Examples of this latter point include:

- non-US holdings of US treasuries reaching $US 7.07 trillion as of December 2020;[23] and

- US dollar-denominated exchange reserves held by foreign (non-US) central banks reaching 60.5% as of the third quarter of 2020.[24]

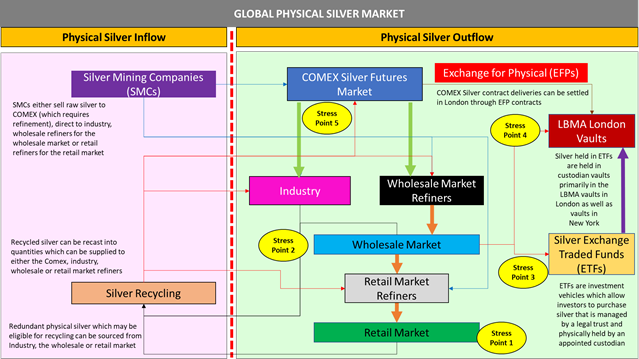

Any additional demand for physical silver, in particular, will carry a material consequence given the extreme tightness that has developed in the global market for physical silver during February 2021, as noted in the article entitled, “The Silver Market Fast Approaches Breaking Point”.[25]

In fact, Diagram 1 from that article (which has been reproduced below)illustrates 5 points of stress across the physical silver market that are likely to worsen if additional monetary stimulus results in sustained additional demand for physical silver.

Diagram 1: Global Physical Silver Market

Cracking the Silver Market Price Ceiling

Added pressure on the physical silver market becomes an intriguing element in the determination of the spot price of silver when the mechanics and structure of the silver market are taken into account.

As noted in recent articles:

- “The undeniable manipulation of the silver market”;[26] and

- “COVID-19 exposes gold and silver price manipulation”;[27]

the current internationally recognised price of silver does not reflect the underlying physical demand and supply fundamentals of the silver market. Rather, the price of silver is being actively supressed by the actions of the New York-based COMEX futures market as well as the London Bullion Market Association (LBMA) and its member organisations (in particular, the bullion banks and bullion refiners).

Moreover, as noted in the article, “George Soros and the Silver Moon Shot” [28], systemic manipulation of the silver market means that, from a market structure perspective, the price of silver is being contained under a price ceiling well below the equilibrium silver price that is multiple times higher than the current price.

Thus, if one accepts the silver market manipulation thesis and if enough pressure is exerted through sustained demand for physical silver via:

- the wholesale and retail markets;

- exchange traded funds (or ETFs); and

- industry

then the spot price of silver is not only likely to rise, but is actually likely to expose the scale to which actual physical silver is mismatched relative to the number of contractual promises of silver ownership and delivery that have been created through derivatives contracts, leasing and rehypothecation.

Exposure of such massive mismatch, which silver analysts (e.g. David Morgan) have claimed may be as high as 1000 paper silver claims for each physical ounce of silver - is likely to result in an astronomical explosion of the spot silver price. This is because institutions that possess unbacked promises to deliver physical silver, particularly at the COMEX, will scramble to obtain as many 1,000-ounce “good delivery” silver bars in order to avoid a default of their contractual delivery obligations.

The central question for industrial consumers and investors of physical silver is whether sufficient and sustained pressure can be exerted on the physical silver market that can break the current manipulated price ceiling.

Austrian economists, based on the writings of economist Ludwig Von Mises, argue that such pressure is all but inevitable. They argue that the general public will, at some future point in time, come to understand that current fiscal and monetary policy settings are caught in a cycle of never‑ending stimulus and that this will lead to a “crack-up boom” resulting in an insatiable demand for all commodities including physical silver.

A “crack-up boom”, as explained on pages 423 - 424 of Von Mises’ book, “Human Acton”[29], is as follows:

“But if once public opinion is convinced that the increase in the quantity of money will continue and never come to an end, and that consequently the prices of all commodities and services will not cease to rise, everybody becomes eager to buy as much as possible and to restrict his cash holding to a minimum size.

For under these circumstances the regular costs incurred by holding cash are increased by the losses caused by the progressive fall in purchasing power. The advantages of holding cash must be paid for by sacrifices which are deemed unreasonably burdensome. This phenomenon was, in the great European inflations of the 'twenties, called flight into real goods (Flucht in die Sachwrte) or crack-up boom (Katastrophenhausse).”

Given that central banks, as noted above, have no intention to allow a deflationary depression to occur, time will tell whether the general public across the world will awaken to the fact of endless and rapid money supply growth and respond accordingly.

The Final Chapter of the COMEX?

Even if a “crack-up boom” was to translate into unprecedented demand for physical silver, perhaps the ultimate stumbling block to a release of the silver price towards true equilibrium will be unnatural interventions by institutions involved in silver market manipulation such as the COMEX futures market itself.

To several American silver analysts, potential unnatural interventions by the COMEX, such as changing market or trading rules) and forcing cash settlement of futures contracts standing for delivery, remain a primary concern.

Such concerns are warranted given that during the silver bull markets of 1980 and 2011, the COMEX in conjunction with the regulatory arms of the US Government intervened to limit the rise of the silver price.

While existing rules give the authorities at the COMEX the ability to manipulate current market and trading rules/settings, any systematic and ongoing attempt to:

- deny counterparties access to physical gold and silver bullion; or

- provide favourable conditions to bullion banks at the expense of investors and producers

whether through:

- amendments to the market rules; or

- forcing counterparties to settle claims in cash

will undermine the legitimacy and ongoing viability of the COMEX as the premier international hub in which gold and silver futures contracts are traded and settled.

The risk that an alternative futures exchange to the COMEX may emerge – one that promises to not abuse their rule‑making capability may act as a sufficient brake on, or deterrent to, any action that prevents the price of silver from moving commensurate with physical demand relative to supply.

Conclusion

With the Biden Administration in power for only five weeks, international anxieties regarding the performance of the US economy, especially with respect to inflation, coupled with the loss of American prestige given reduced confidence in American political institutions has now triggered the start of a bond market crisis through an aggressive sell off of existing US Treasuries and weak demand for newly-auctioned bonds.

This crisis has now spread across the world to other bond markets among developed nations.

The explosive nature of rising bond yields has the potential to threaten the stability of the global financial system and economy, given the size and nature of the current global debt bubble coupled with the risky financial derivatives that are now so pervasive across the world.

Thus, given the Biden Administration’s twin goals of aggressive economic stimulus and financial stability, the only recourse for American policy makers (including the US Federal Reserve) in the immediate future is evermore expansion of the money supply and the balance sheet of the US Federal Reserve – not dissimilar to their response in March 2020 to the onset of the COVID-19 pandemic.

This is also true for other jurisdictions such as Australia, Japan and Europe.

Despite attempts by central bank officials to downplay (and in some cases conceal) the risk of inflation, evident signs of stagflation whether in the US or around the world will likely lead foreign investors to rapidly lose confidence in fixed-income financial assets such as bonds as well as fiat currencies.

The flight away from fiat currencies (such as the US dollar) into hard forms of money (such the physical gold and silver bullion) will exert additional pressure in both gold and silver markets, drying up necessary physical supply required to settle contractual delivery requirements, especially in the COMEX futures market.

In the context of the silver market, the end game question to the current bond market crisis is whether sufficient pressure can be applied that breaks the price manipulation regime with the effect of releasing the silver price from its current price ceiling.

In such an event, the price of silver will shoot up to its unmanipulated equilibrium price.

Economists belonging to the Austrian school of economic thought believe that the psychological power of a ‘crack-up boom’ when manifested at a global level will be sufficient to overpower the institutions and mechanisms involved in the market manipulation of silver, including the COMEX.

Given the global nature of commodity markets in the 21st Century, any attempt to manipulate the COMEX’s market and trading rules to benefit either the US Government or American financial institutions will undermine the COMEX’s legitimacy and threaten its ongoing viability as the world’s focal point for trading silver market futures.

The risk of destroying the COMEX’s international credibility may be the key determining factor that finally liberates the global price of silver.

John Adams is the Chief Economist for As Good As Gold Australia

[1]https://www.adamseconomics.com/post/the-biden-administration-will-accelerate-stagflation

[2] https://www.cnbc.com/2021/02/25/us-bonds-treasury-yields-rise-ahead-of-fourth-quarter-gdp-update.html

[3] https://www.zerohedge.com/markets/treasury-yields-soar-after-catastrophic-tailing-7y-auction

[4] The ‘bid-to-cover ratio’ is the dollar amount of bids in a treasury auction vs the dollar amount of bonds sold at the auction. The ‘bid-to-cover ratio’ is an indicator of the demand for US Treasuries.

[5] https://www.zerohedge.com/markets/australias-yield-curve-control-verge-collapse

[6] https://www.zerohedge.com/markets/japanese-10y-blows-out-above-ycc-barrier-us-yields-are-already-sliding

[7] https://www.afr.com/policy/economy/rba-doubles-daily-bond-buying-to-4b-20210301-p576nr

[8] https://www.aofm.gov.au/intermediaries/securities-lending-facility

[9] https://www.afr.com/wealth/personal-finance/worst-bond-blood-bath-since-1994-20210225-p575nn

[10] https://www.afr.com/policy/economy/rba-expands-qe-by-100bn-upgrades-employment-20210201-p56yj6

[11] https://www.rba.gov.au/media-releases/2021/mr-21-03.html

[13] https://www.reuters.com/article/eurozone-bonds/update-3-german-bonds-recover-still-set-for-steep-monthly-selloff-idUSL1N2KW0P2

[14] https://www.zerohedge.com/markets/begging-fed-guidance-bofa-expects-fed-address-bond-rout-soon-coming-week

[15] https://www.smh.com.au/business/the-economy/the-crash-is-going-to-be-violent-italy-headed-for-crisis-warns-banker-20181029-p50ckf.html

[16] https://www.cnbc.com/2019/01/04/fed-chief-powell-just-walked-back-his-autopilot-remark-and-the-financial-markets-love-it.html

[17] https://www.afr.com/policy/economy/debt-cost-spike-presents-a-few-challenges-for-rba-20210228-p576g7

[18] https://www.bloomberg.com/news/articles/2021-02-09/surging-inflation-may-force-fed-to-resort-to-yield-curve-control

[19] https://www.kitco.com/news/2021-02-17/Is-yield-curve-control-around-the-corner-as-gold-price-faces-a-tsunami-of-bad-news.html

[22] https://www.icmagroup.org/Regulatory-Policy-and-Market-Practice/Secondary-Markets/bond-market-size/#:~:text=The%20SSA%20bond%20markets%20are,the%20global%20outstanding%20SSA%20market.

[23] https://ticdata.treasury.gov/Publish/mfh.txt

[24] https://wolfstreet.com/2020/12/31/us-dollar-as-global-reserve-currency-amid-feds-qe-and-us-government-deficits-dollar-hegemony-in-slow-decline/

[25] https://www.adamseconomics.com/post/the-silver-market-fast-approaches-breaking-point

[26]https://www.adamseconomics.com/post/the-undeniable-manipulation-of-the-silver-market

[27]https://www.adamseconomics.com/post/covid-19-exposes-gold-and-silver-price-manipulation

[28] https://www.adamseconomics.com/post/george-soros-and-the-silver-moon-shot