AUD

AUD

Loading... Please wait...

Loading... Please wait...

Recent Posts

Conquering Silver Market Manipulation

Posted by on

Conquering Silver Market Manipulation

Across the world, frustration is growing among silver market participants resulting from the price action over the past two years (2020 – 2022).

During this period, extraordinary monetary and fiscal stimulus in response to the COVID-19 pandemic, supply chain disruptions as well as the Russia-Ukraine war has resulted in explosive, multi‑decade record levels of official rates of inflation, leading to many economies experiencing stagflation.

As a result, the prices of commodities, real estate, public-listed shares and cryptocurrencies have seen significant increases (consistent with the wealth effect), although these assets have witnessed a dramatic pullback during April-May 2022 as major central banks, such as the US Federal Reserve, have begun to tighten monetary policy through the lifting of official interest rates.

However, during the same period, the price of silver has been effectively capped at $US 30 per troy ounce, primarily trading between $US 22 - 28 per troy ounce as shown in Diagram 1.

Specifically, since the commencement of the COVID-19 pandemic, where the price of silver reached a low of $US 11.63 per troy ounce on 16 March 2020, silver has only approached $US 30 per troy ounce on two occasions – that being $US 29.63 on 3 August 2020 and $US 30.09 on 1 February 2021.

Diagram 1: Silver Market Price Chart (2018 – 2022)[1]

Given the:

- current macroeconomic context;

- geo-political conditions; and

- the price action experienced in non-precious metals commodities

the silver price action during 2020 - 2022 strongly suggests prima facie evidence of market manipulation. Importantly, this new evidence adds to the body of market manipulation evidence as outlined in the January 2020 article “The Undeniable Manipulation of the Silver Market”[2]and the May 2020 article “COVID-19 exposes gold and silver price manipulation”[3].

Specifically, the former article points out the key fact that silver has yet to surpass its January 1980 high, expressed in Australian dollar terms, even though Australia has witnessed an explosion in its money supply from January 1980 to December 2019 by approximately 2,600% while the above‑ground stock pile of silver grew by just 94.2% over the same period.

Silver Market Manipulation

Importantly, real world examples exist which strongly suggest that manipulation of the silver market occurs across the entire supply chain and pricing structure, including:

- the physical market (i.e., wholesale market, major institutional holdings such as central banks (e.g., Bank of England) as well as the retail market);

- the Over-the-Counter (OTC) markets (i.e., London, United Kingdom); and

- the futures derivatives exchanges (i.e., Comex, United States of America).

A diagrammatical illustration of the silver market, which encompasses both the physical market and the pricing structure is demonstrated in Diagram 2[4].

Diagram 2: Global Physical Silver Market

Such real-world examples of manipulation in precious metals markets include:

- settlement of a class action lawsuit in December 2021 to the tune of $US 152 million by multiple financial institutions (including Barclays Bank PLC, Scotiabank, Société Générale, and the London Gold Market Fixing Ltd) to end claims that they illegally fixed prices on the gold market[5] (noting that Deutsche Bank and HSBC settled similar claims in 2016[6]);

- JP Morgan found guilty and fined $US 920 million in 2020 by the US Department of Justice for manipulating precious metals markets via the practice of ‘spoofing’[7][8];and

- Morgan Stanley settling a $US 4.4 million class action in 2007 for failure to purchase and store physical silver on behalf of investment clients[9].

Market Manipulation - Emphasis and Analysis

Within the English-speaking world, discussion and analysis of precious metals market manipulation is dominated particularly by American and Canadian analysts.

These analysts tend to place significant emphasis on the futures market (i.e., the COMEX and its regulator, the Commodity Futures Trading Commission (CFTC)) at the expense of focusing on manipulation practices within the physical market.

Such overemphasis is understandable given that:

- the COMEX and the CFTC are American institutions; and

- some Comex data is made public, whereas there is little available data of physical OTC trading and storing (ETFs, pools, certificates, etc).

Nevertheless, manipulation within the physical market, which includes fraudulent fractional reserve and rehypothecation schemes (including leasing/swaps, etc), are of critical and material importance.

The market effect of such scheme is to artificially expand the supply of silver and thus contribute to price suppression.

Moreover, at the heart of these physical market manipulation schemes are a lack of integrity in:

- product quality (i.e., fake or diluted bars (e.g., bullion bars which are not at least 99.9% pure));

- storage custodian services (which includes unallocated and pool-allocated products); and

- audit quality.

Traditional Precious Metals Analytical Model

Importantly, the existence of multiple forms of market manipulation renders the conventional forms of precious metals analysis redundant.

For the overwhelming majority of economically trained analysts, precious metals analysis proceeds according to the following phases:

- Phase 1 - central bank prints fiat currency (either physical or digital units of currency);

- Phase 2 - this leads to inflation and currency devaluation;

- Phase 3 - this leads to economic agents shifting capital from fiat currency to assets which act as a store of value (primarily precious metals);

- Phase 4 - this shift of capital generates additional investment demand for precious metals; and

- Phase 5 - additional investment demand drives the price of precious metals higher ceteris paribus (i.e., all other things remaining equal).

In particular, this investment demand price driven model (as described above) has been promoted aggressively by precious metals (including silver) market commentators/analysts on alternative platforms such as YouTube, and particularly by those who are linked to retail bullion dealerships and other related precious metals businesses (including financial institutions who offer precious metals related investment vehicles).

These analysts have an inherent conflict of interest given that:

- investment demand price driven model encourages bullion sales as investors believe that their purchase contributes to investment demand and ultimately higher prices; and

- they typically draw remuneration via commissions on bullion sales.

Nevertheless, to test whether this model reflects real world events within the silver market, both the price behaviour as well as data from the physical market need to be considered.

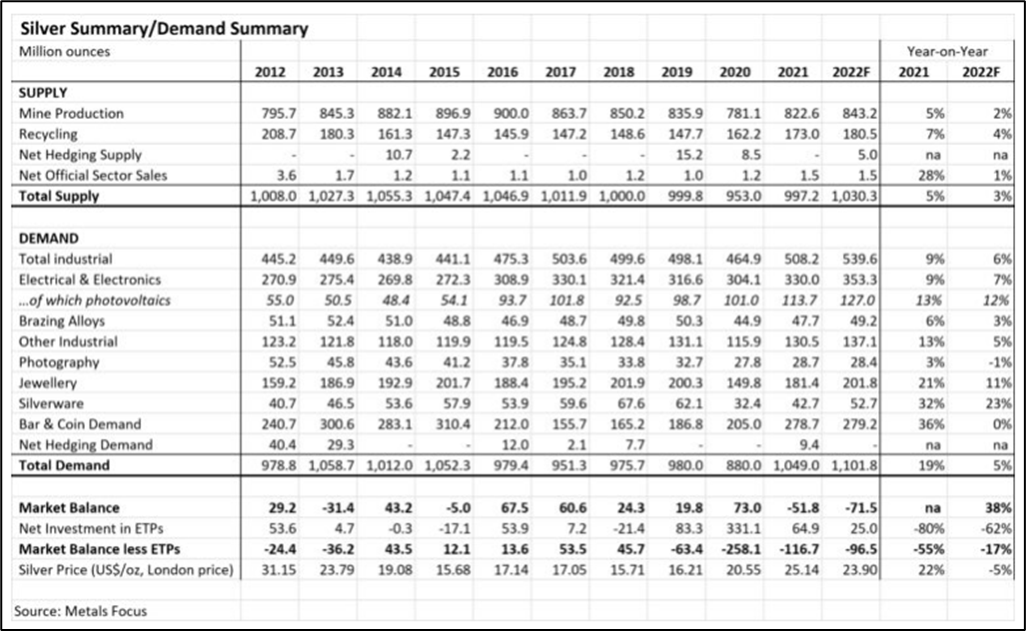

Market data from the Silver Institute (as shown in Table 1 below), demonstrate that:

- Industrial silver demand was the highest on record in 2021 (508.2 million troy ounces) and is projected to reach a new high in 2022 (539.6 million troy ounces);

- retail silver investment demand in the form of bars and coins in 2021 (278.7 million troy ounces) and forecasted for 2022 (279.2 million troy ounces) are the highest since 2015;

- while net investment demand via Exchange Traded Products (ETPs) reached a record in 2020 (at 331.1 million troy ounces), net ETP demand in 2021 and forecasted for 2022 remain positive (i.e., net inflows) at 64.9 and 25 million troy ounces respectively, although slowing; and

- the global physical silver market experienced a net annual market balance deficit in consecutive years of 2019 (63.4 million troy ounces), 2020 (258.1 million troy ounces) and 2021 (116.7 million troy ounces) and is projected to experience another net annual deficit in 2022 (96.5 million troy ounces) when factoring in all forms of industrial and investment (retail and ETP) demand.

These facts paint a strong fundamental picture for why the price of silver should have risen over 2020 – 2022 consistent with other commodities such as base metals, energy and agricultural goods.

Table 1: Silver institute’s Global Silver Market Data[10]

However, when considering both:

- data from the Silver Institute; and

- the silver price behaviour of 2020 – 2022;

the conventional model of precious metals markets analysis from both a broader macroeconomic as well as microeconomic market perspective does not reflect real world events – meaning that increased silver demand during an inflationary period does not necessarily lead to a higher silver price. Thus, an alternative explanation of how the silver market operates is now required.

Alternative Market Thesis

While, as noted above, fraudulent derivative trading practices (such as spoofing) do exist and can play a significant role in how price is manipulated via the COMEX, fractional reserve and rehypothecation (via leases/swaps, etc) schemes that materially distort the real state of the physical market also play a significant role.

In contrast with the traditional (5 phase) analytical model outlined above, major systemic fraud in the physical market results in investment demand having little influence on market price.

For example, if an additional $US 1 billion of investment demand for physical silver entered the market, but this investment was not actually backed by physical silver (even if the investor believed it to be), then this flow of fiat currency capital would have little to no effect on market price (as supply is assumed to have, in effect, automatically and equally responded, regardless if true or not – and without the credible threat of objective oversight/audit and penalty by independent authorities).

Thus, a reasonable, alternative explanation regarding the dynamics of the silver market suggests that the silver price is driven more by investment supply (i.e., real changes in supply) and not so much in investment demand (or the extent to which investment demand is actually backed by physical silver bullion).

In the most extreme case, infinite fractional reserve supply (i.e., supply of silver bullion which physically doesn’t exist) renders investment demand completely irrelevant as a price influencer.

New Approach to Rectifying Silver Market Manipulation

If systemic manipulation of the silver market is acknowledged - both within the derivative and physical markets - the question then becomes: what is the appropriate mechanism in order to best address this manipulation and restore the market back to its natural demand and supply forces?

Unfortunately, given the inherent political and legal difficulties of seeking redress in countries such as the United States of America and the United Kingdom (given the potential involvement of both governments in precious metals market manipulation), retail investors, analysts and commentators have little prospect of overcoming institutional resistance and market inertia in:

- Washington DC (CFTC/DOJ);

- New York (COMEX); or

- London (OTC Market and the Bank of England).

Thus, there is little hope that market manipulation can be tackled by attempting to expose and end the corrupt market practices at the futures derivatives market (i.e., COMEX) by market participants such as the Bullion Banks and those regulators who are charged with governing them such as the CFTC (i.e., the top-down approach).

Rather, the only available strategy to address manipulation of the silver market is through a bottom‑up approach that seeks to address instances of fraud and rehypothecation in the physical market. This includes unallocated and pool-allocated schemes offered within the retail market to retail investors (e.g., the Perth Mint).

Exposure and rectification of such fraud and rehypothecation will shrink supply from the “market‑understood” quantity of supply to the “actual” quantity of supply.

Importantly, there are reasonable grounds to assume that there are sufficient levels of fraud and rehypothecation within the physical silver market to have a material impact on the function of the silver market and thus the silver price set by the COMEX and the OTC market.

Addressing physical market fraud and rehypothecation schemes will ultimately put pressure on the OTC market and futures exchanges and will ultimately drive price higher when major markets and exchanges get raided for physical silver in similar fashion to what happened to nickel at the London Metals Exchange in March 2022.

Ideally, what is required is exposure of a sizeable fraud or rehypothecation scheme in the physical silver market to cause a sufficient number of market participants to trigger a rush of redemptions which would expose other similar schemes across the world.

Such an event would likely guarantee that the price of silver will break through the current $US 30 per troy-ounce price ceiling towards the upside.

Conclusion

From all the objective evidence available, it is now quite obvious that the price behaviour within the silver market over the past two years (2020 – 2022) makes little market or economic sense instead, market manipulation offers a more compelling explanation.

Despite historical attempts to address such manipulation, all previous attempts (especially those involving large financial institutions – i.e., the bullion banks) have either failed or resulted in cash settlements with no admission of wrong-doing, thus providing little incentive for market participants to alter their behaviour.

Rather, in order to effectively address market manipulation, what is required is a paradigm shift in approach and execution.

This article argues that the only salvation for silver investors is to expose fraud and rehypothecation schemes within the physical market which, in turn, exerts pressure on derivative exchanges via a bottom-up approach.

Exposure of a sufficiently large scheme that proves scandalous is likely to trigger an international chain reaction that expedites the process of squeezing derivative futures markets and manifesting in a higher, less manipulated, silver price.

John Adams is the Chief Economist for As Good As Gold Australia

[1] Source: https://silverprice.org/

[2] https://www.adamseconomics.com/post/the-undeniable-manipulation-of-the-silver-market

[3] https://www.adamseconomics.com/post/covid-19-exposes-gold-and-silver-price-manipulation

[4] This diagram was sourced from the John Adams article, “The silver market fast approaches breaking point”. See the following link: https://www.adamseconomics.com/post/the-silver-market-fast-approaches-breaking-point

[5] https://www.gata.org/node/21570

[6] See footnote 5.

[7] Spoofing according to the US Department of Justice means: “In tens of thousands of instances, traders on the precious metals desk placed orders to buy and sell precious metals futures contracts with the intent to cancel those orders before execution, including in an attempt to profit by deceiving other market participants through injecting false and misleading information concerning the existence of genuine supply and demand for precious metals futures contracts”.

[8] https://www.nasdaq.com/articles/jpmorgan-to-pay-%24920-mln-fine-for-manipulating-precious-metals-treasury-market-2020-09-29